The Centre is planning to make it obligatory for medical health insurance firms to approve cashless authorization requests inside an hour, and ultimate declare settlement requests inside three hours, based on two folks near the event.

Alongside, an expert company could also be employed to design standardized insurance coverage declare and software kinds which might be simple to grasp and fill. Such kinds would additionally be certain that insurance coverage firms settle claims in full and inside the specified interval.

“The concept is to have BIS-type requirements within the insurance coverage sector that streamline the operations of the medical health insurance trade,” stated one of many officers cited above on the situation of anonymity. BIS or Bureau of Indian Requirements is the nationwide requirements physique of India.

Additionally learn | Insurance coverage premiums are rising rapidly. Here is how one can get a reduction.

The official added that the target is to convey extra folks underneath medical health insurance protection in order that “insured sufferers don’t face monetary misery as a result of rising medical payments”. That is in step with the Union authorities’s purpose to offer reasonably priced medical health insurance protection and insurance coverage to all by 2047, which Irdai had introduced in November 2022.

To make sure, the insurance coverage sector’s regulator—Insurance coverage Regulatory and Growth Authority of India (Irdai)—had issued a grasp round in 2024 with particular tips for well timed decision of declare settlement requests. Nevertheless, well being insurers going through a surge in claims have failed to stick to the laws.

“There have been circumstances of insurers rejecting or denying 100% cashless claims,” the official cited earlier stated. “Strict enforcement of Irdai’s laws and the standardization of the settlement course of ought to assist enhance shopper confidence in medical health insurance merchandise.”

Queries emailed to the Union finance ministry and Irdai remained unanswered until press time.

Learn this | Insurance coverage legal guidelines invoice set for monsoon session, proposes 100% FDI, composite licenses and sweeping reforms

The transfer to quicken the method of approvals from insurance coverage firms is along with the Centre’s efforts to strengthen the Nationwide Well being Claims Change (NHCX) together with the Nationwide Well being Authority and Irdai. The NHCX is a digital platform designed to streamline and standardize the processing of medical health insurance claims by insurance coverage firms.

As of July 2024, 34 insurers and third-party directors (TPAs) have been dwell on the NHCX, and roughly 300 hospitals have been ramping as much as begin sending their claims on the platform. To make sure, India has 26 common insurance coverage firms, two specialised insurers, and 7 standalone medical health insurance firms, and a a lot larger depend of hospitals working into an estimated 200,000 in quantity.

Not really easy

Insurance coverage trade insiders lauded the transfer to hasten approvals however pointed to on-ground challenges. A high govt of a personal sector common insurer, requesting to stay nameless, stated the thought would certainly promote higher participation of individuals in medical health insurance. “Nevertheless, the federal government must also look into elements of rising healthcare payments that always make fast declare settlement tough,” this govt stated. “The standardisation of declare kinds could be a very good step, however its enforcement must be ensured.”

In keeping with common insurer ACKO’s India Well being Insurance coverage Index 2024, the typical declare dimension in medical health insurance insurance policies rose 11.35% in 2023, reflecting the rise in healthcare prices and medical inflation. This rise in medical inflation is resulting in larger medical health insurance premiums which have nearly doubled in previous three to 4 years. Additionally, the report pointed to an annual 14% fee of enhance in healthcare prices in India.

Additionally learn | Who will get the insurance coverage payout—nominee or authorized heirs?

R. Balasundaram, secretary common of the IBAI (Insurance coverage Brokers Affiliation of India), pointed to extra challenges. “It’s one factor to move a regulation however completely a distinct problem on implementation,” he stated. “Insurers/TPAs/ hospitals have their very own sensible points that are available in the best way of assembly these timelines. It is just a intently co-ordinated effort between these stakeholders that may crunch the timelines for concluding a declare.”

Balasundaram added {that a} claimant is just involved about how rapidly a TPA (third-party administrator) approves a declare and the way quickly he can come out of hospital after affirmation of the settlement quantity.

“Claimant is probably not bothered in regards to the time taken for insurer to settle with the hospital,” he stated. “Nevertheless, that is most necessary for hospitals and insurers too. It’s work in progress. We’re on the correct path, although progress is gradual. Linking this on to growth of medical health insurance protection could be a bit untimely.”

“Fast settlement of cashless claims is essential,” stated C.R. Vijayan, former secretary common of Normal Insurance coverage Council. “Hospital discharge usually occurs within the night. Payments are despatched by hospitals to insurance coverage firm/TPA. They get an hour or so to reply. Throughout this time affected person/bystander is anxious about when the declare will probably be settled and the way a lot. The present system must be revamped and made extra clear. Standardisation of declare kinds and so on. will assist.”

Additionally learn | Indian insurtech startups look abroad as AI reshapes international insurance coverage

Sharad Mathur, managing director and chief govt officer of Common Sompo Normal Insurance coverage, was in favour of the federal government’s transfer. “Sooner declare registration and settlement timelines, if applied successfully, will cut back stress on sufferers and their households whereas additionally strengthening belief within the insurance coverage course of,” he stated, including that standardized surgical procedure charges and discharge documentation throughout hospitals can streamline backend operations and decrease disputes, enabling insurers to course of claims swiftly and precisely.

“Such alignment between healthcare suppliers and insurers will undoubtedly end in a smoother expertise for policyholders. If mandatory, bringing hospitals underneath regulatory oversight would help attaining the bigger goal,” he added.

The central authorities has additionally been engaged on having a separate regulator for the medical health insurance enterprise. Final 12 months, the Union finance ministry wrote to the Union well being ministry to finalize the contours of the brand new regulator for the well being sector to result in uniformity in well being companies and facilitate reasonably priced medical health insurance protection for all residents. Nevertheless, the plan continues to be in works and has not moved ahead.

Low penetration

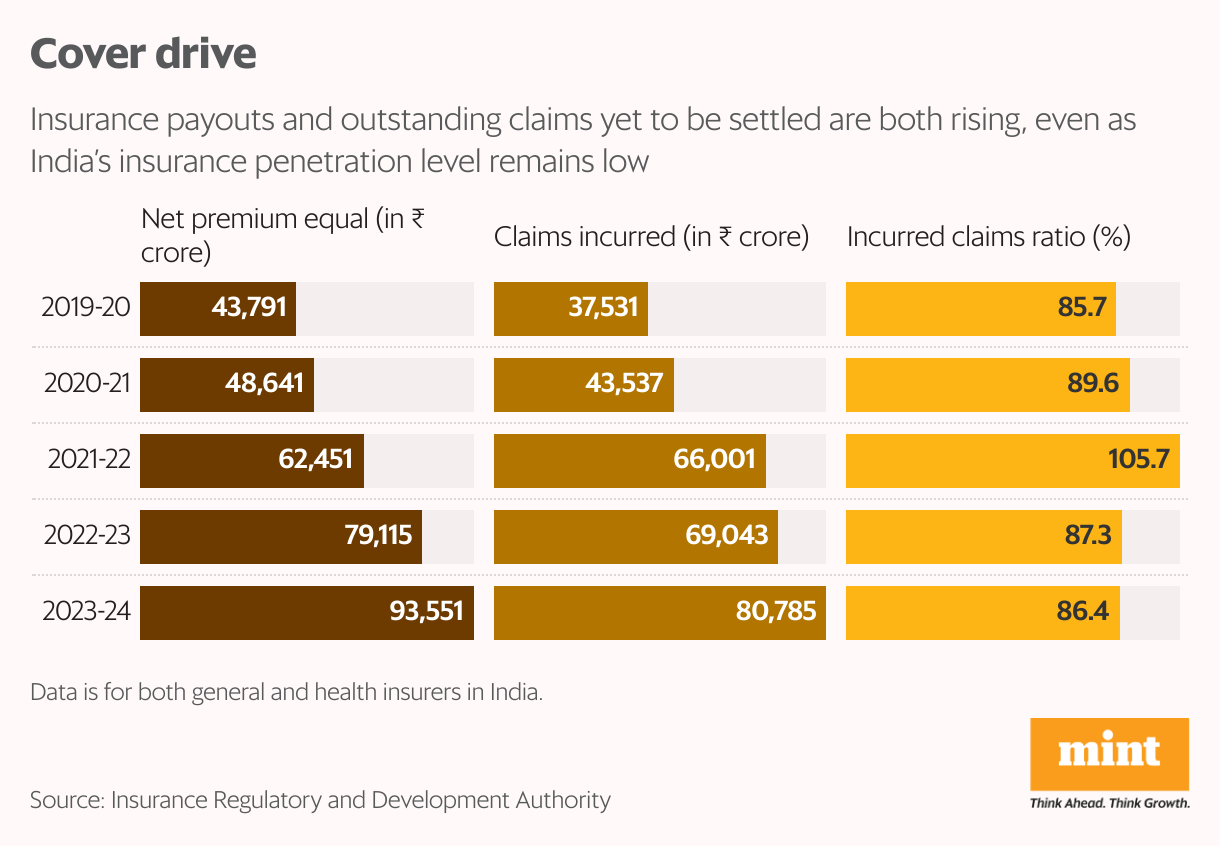

The newest growth comes within the backdrop of rising payouts for insurance coverage claims in addition to the variety of excellent claims but to be settled. In keeping with Irdai, the gross direct premium underwritten by common insurers in FY25 (April to November) stood at ₹2,05,138 crore, a progress of 8.89% over the identical interval of earlier fiscal ( ₹1,88,386 crore).

Learn this | Insurance coverage surety bonds proposed to be added as assure instrument for pipeline, metropolis fuel initiatives

As for excellent claims, information from Irdai exhibits there have been 25 million excellent claims as of March 2024. This was a major rise in comparison with 17.5 million in March 2023, which in flip had greater than doubled from 8.5 million excellent claims in March 2022.

India’s healthcare expenditure stays low in comparison with the worldwide common. In keeping with the World Well being Group’s International Well being Expenditure Database, India’s healthcare spending as a share of gross home product (GDP) is considerably decrease than that of developed nations just like the US and the UK, in addition to creating international locations similar to Brazil, Nepal, Vietnam, Singapore, Sri Lanka, Malaysia, and Thailand.

Between 2013-14 and 2022-23, complete insurance coverage penetration rose from 3.9% to 4%, whereas insurance coverage density rose from $52 to $92.

Insurance coverage penetration and density are used to evaluate a rustic’s stage of growth of the insurance coverage sector. Insurance coverage penetration is measured as the share of insurance coverage premium to GDP, and insurance coverage density is calculated because the ratio of premium to inhabitants (per capita premium).

And browse | How one can get a mortgage in opposition to an insurance coverage coverage

Shashwat Alok, affiliate professor of finance at Indian College of Enterprise (ISB) stated, “Insurance coverage protection penetration in India stays concerningly low, at the least partly as a result of shoppers stay unsure whether or not their claims will probably be honoured in occasions of want. The opposite points are lack of know-how and affordability. So, the proposed laws are well-intentioned and well timed. The emphasis on accelerating registration and settlement of medical health insurance claims addresses a important problem confronted by shoppers and might foster higher belief and shopper confidence within the insurance coverage trade. This will, in flip, encourage elevated shopper participation in insurance coverage markets by beforehand uninsured/underinsured shoppers, and assist increase the shopper base of insurance coverage corporations, leading to a win-win for all concerned.”

“Over time, the growth in shopper base can permit insurers to cost medical health insurance merchandise extra competitively as a result of elevated threat diversification throughout a bigger variety of prospects, leading to higher affordability. Nevertheless, the effectiveness of those modifications will hinge on clear accountability frameworks to make sure insurers and hospitals adhere to the proposed timelines. Additional, such modifications must be mixed with parallel coverage measures addressing affordability and consciousness,” he added.

==================================================

AI GLOBAL INSURANCE UPDATES AND INFORMATION

AIGLOBALINSURANCE.COM

SUBSCRIBE FOR UPDATES!