Among the many raft of Cupboard selections introduced final week, the one to increase the Ayushman Bharat medical insurance scheme to all residents aged 70 years and above, regardless of revenue, was the largest headline-grabber.

The Pradhan Mantri Jan Arogya Yojana at present gives a ₹5 lakh well-being cowl to the underside 40% of India’s inhabitants. The Centre reckons that the growth will profit around 60 million senior residents, with an outlay pegged at ₹3,437 crore.

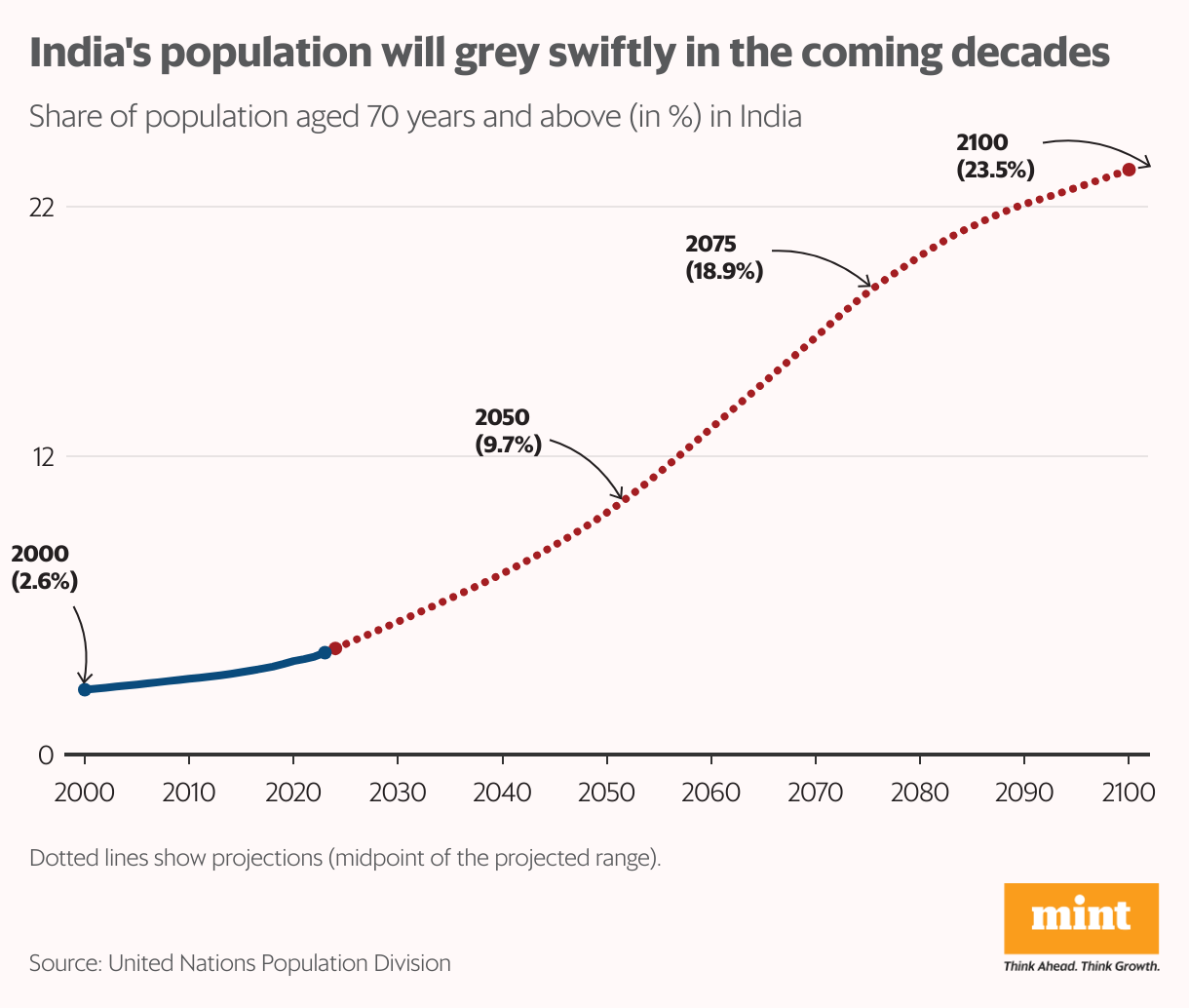

The transfer comes at a time when India’s inhabitants are about to gray sooner than ever earlier than. An estimated 4.3% of India’s inhabitants is over 70, with the share projected to rise to 9.7% by 2050, in response to the United Nations. Well-being occasions happen at an extra speedy price among the many aged. As they’re extra prone to have pre-existing circumstances, insurance coverage corporations cost them a hefty premium and cover them with extra exclusions. All of this makes the federal government’s transfer well-timed.

Additionally learn: Why GST Council can not ignore the medical insurance row.

Since its inception in 2018, the Ayushman Bharat medical insurance scheme has catered to 68.6 million hospital admissions price ₹90,204 crores, in response to the well-being ministry, with almost an equal cut up between women and men, and 30,510 impaneled hospitals, as per official information.

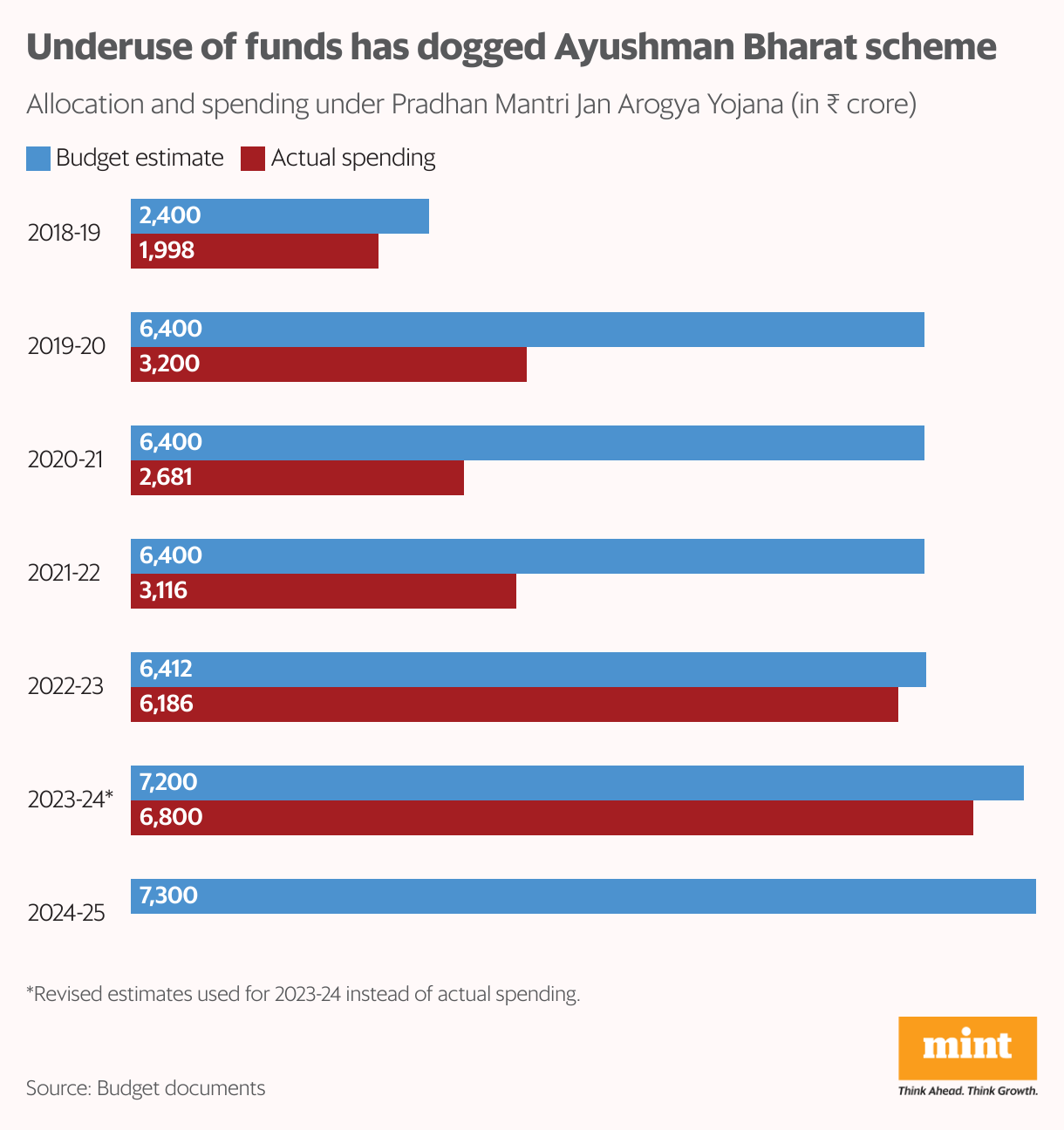

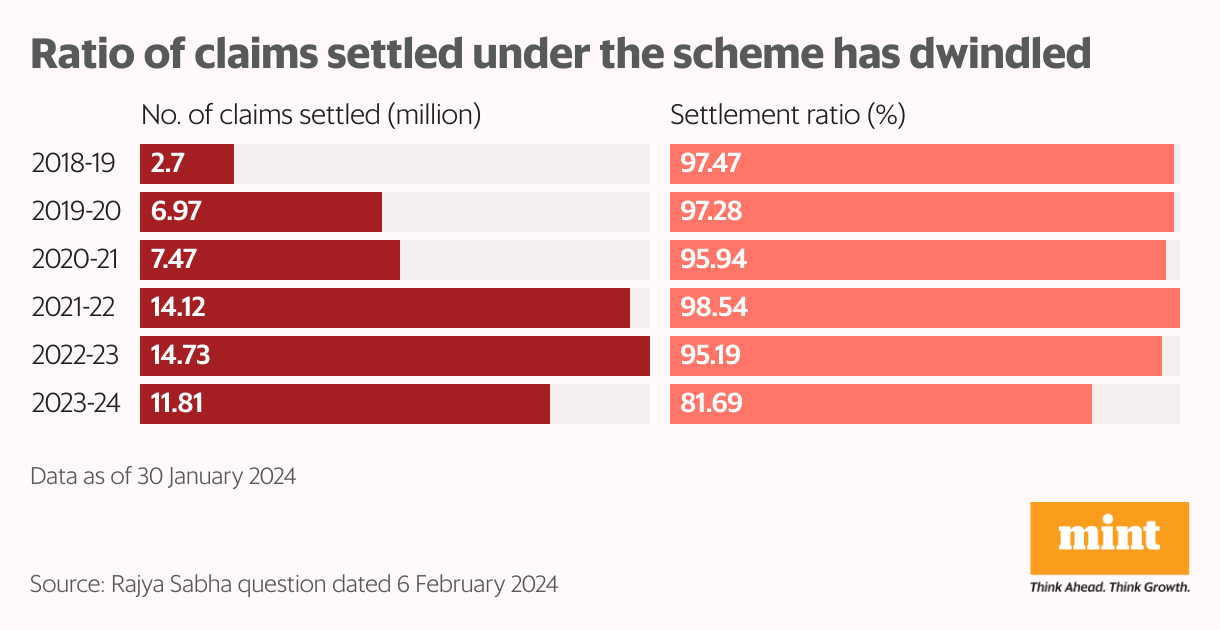

But, for all its claimed successes, cracks are seen. The scheme has suffered constant gross underutilization of funds, and the claims settlement ratio has fallen from 97.5% after launch to 81.7% in 2023-24, authorities information present. This raises questions on whether or not the scheme can successfully deal with an extra quantity of beneficiaries.

Disconcerting points

The Ayushman Bharat scheme confronted teething implementation points, such as the exclusion of eligible beneficiaries and delayed declaration processing, as highlighted by the Comptroller and Auditor Normal and a parliamentary panel on well-being. Beneficiaries, in some circumstances, have been compelled to pay for therapy regardless of the scheme offering cashless providers, the CAG noticed.

Specialists point out that the success of the scheme hinges on well-timed funds to hospitals and aggressive charges to lure personal suppliers. Delayed funds have disincentivizedimpaneledd personal suppliers, prompting them to curtail providers to beneficiaries, Mint had earlier reported.

A disadvantage of the Ayushman Bharat scheme is that it provides solely free inpatient care; outpatient hospitalization providers will not be lined though this has a far better demand and want.

Medicines accounted for about 29% of the out-of-pocket expenditure for inpatients and 60% for outpatients in India, in response to a 2022 research led by Mayanka Ambade of the Worldwide Institute for Inhabitants Sciences.

Expertise from aging international locations globally additionally exhibits that the necessity for outpatient care—and consequently bills—is increased for weak populations such as the aged and chronically in poor health. As non-communicable illnesses shoot up in India, outpatient visits may take up a giant pie of well-being expenditures for the aged rather than hospitalization.

Two to tango

Insurance coverage cowl is just one of two elements of the Ayushman Bharat scheme, the opposite being a revamp of current main healthcare centers to encourage illness prevention. The scheme can succeed solely when each elements complement one another effectively. Public well being specialists level out that insurance coverage payouts will enhance and not using a concurrent discount in morbidity except the first well being facet is strengthened.

Research has proven a combined effect of the Ayushman Bharat insurance coverage cowl on out-of-pocket expenditure.

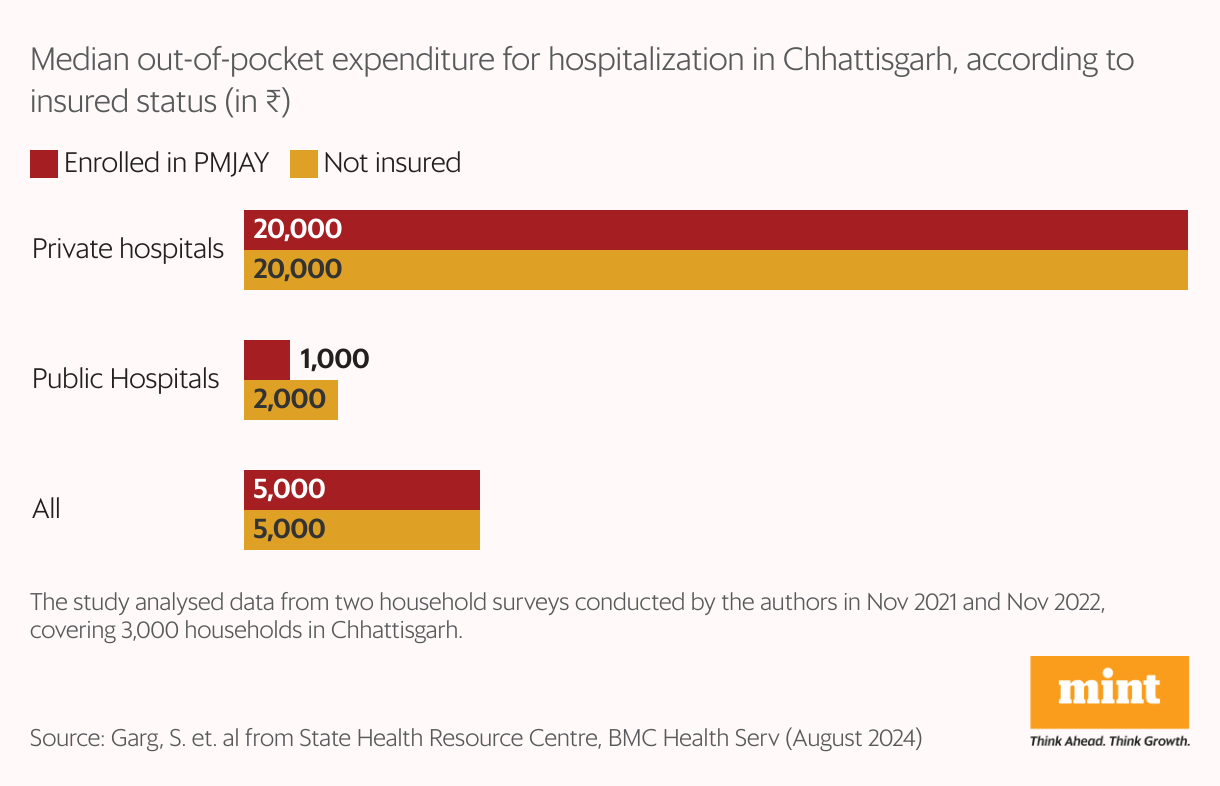

Research in Chhattisgarh by the State Well Being Useful Resource Centre, a technical company offering help to the state authorities, confirmed “little distinction in OOPE for sufferers enrolled within the scheme and the non-insured”, with personal hospitals being dearer.

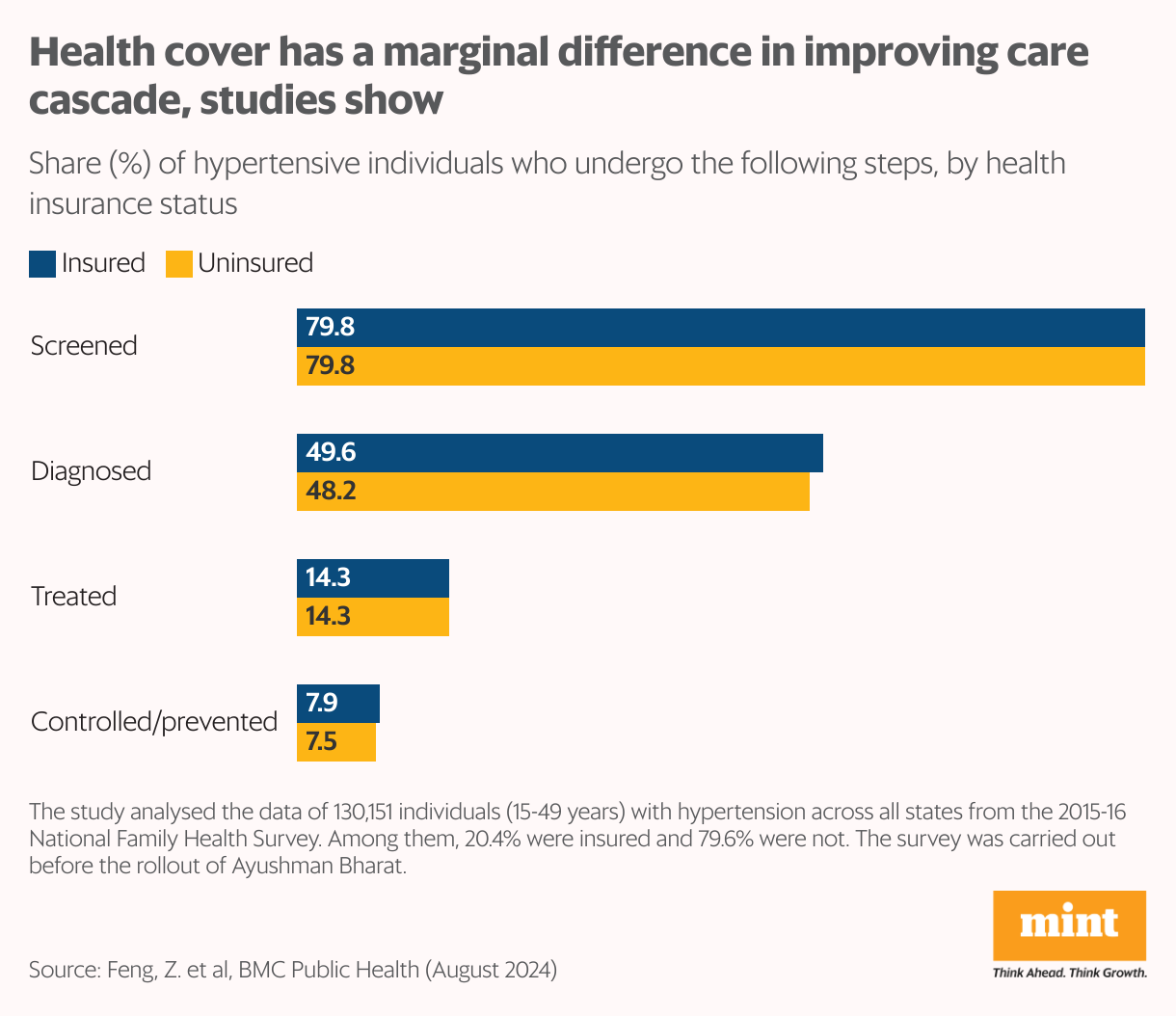

One other research-based mostly on Nationwide Household Wellbeing Survey information discovered the minimal effect of medical insurance on well-being outcomes for hypertensive Indians. It is because having a well-being cowl alone can not assure improved care—an actuality any extension of the scheme should acknowledge.

==================================================

AI GLOBAL INSURANCE UPDATES AND INFORMATION

AIGLOBALINSURANCE.COM

SUBSCRIBE FOR UPDATES!